FinTech leader in the European Union in terms of revenue in 2023

Your company is already operating in Germany and you would now like to export worldwide?

Europe’s Largest Private Customer Market

75% of Germany’s population use FinTech services (higher than the European average of 64%)

Digitalization Potential of German SMEs

39% of Germany’s 3.5 million SMEs – the backbone of Germany’s economy – are interested in integrated financial services.

Favorable Scale-up Market

The industry's market opportunities and the investment focus on growth financing in the FinTech sector favor the above-average growth of German FinTechs from startups to scaleups.

Partnership with Established Financial Sector

The potential for cooperation with established financial sector actors is significant. FinTech companies in Germany have, on average, 13 collaborations with established companies and are thereby able to benefit from existing licenses and access to customer bases. Start-ups typically have seven collaborative partnerships with established companies.

Growing opportunities in Germany’s FinTech Industry

Increasingly Mature Market

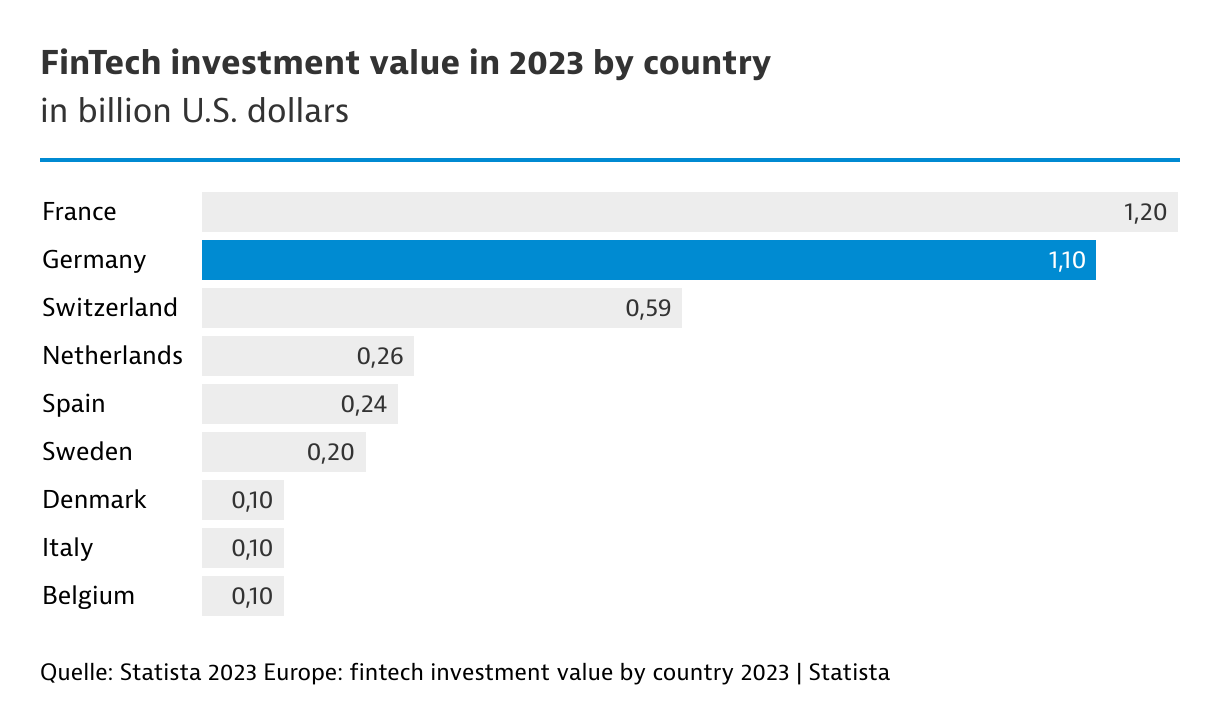

Germany’s FinTech market is characterized by its increasing maturity. The FinTech sector has been one of the best-funded start-up sectors in Germany for years. According to the EY Startup Barometer, the banking (EUR 257 million), payments (EUR 73million) and insurance (EUR 90 million) market segments secured the most VC financing in 2024. In contrast to other European countries, investments in Germany are increasingly focused on late-stage financing. German FinTechs are typically larger and have a higher turnover than general start-ups in the country.

Diverse Sectors, Products and Services

German FinTech companies are active in a wide range of sectors with different products and services. Although the best-known and largest German FinTech companies are predominantly active in the B2C sector and benefit from the high FinTech adoption rate of the largest private customer market in Europe – two thirds of FinTech revenue is generated by B2B business models.

Growing SME Demand

There is also a growing and still underserved demand for FinTech solutions among the approximately three million SMEs in Germany. Here, the digitalization of internal financial processes and the integration of customer payment options are playing an increasingly important role in maintaining market competitiveness.

Banking-as-a-Service and Open Finance Solutions

Demand for banking-as-a-service and open finance solutions for new FinTech business models is also continuing, as is the increasing demand for cybersecurity and fraud prevention solutions. Increased environmental, social and governance (ESG) obligations for companies in Europe are also stimulating demand potential for sustainable financing solutions.

Blockchain Key Technology

Blockchain remains a key technology for digital financial services. According to Statista Market Insights, there are already 27 million users of digital assets (cryptocurrencies, digital tokens, non-fungible tokens) in Germany. This base will account for around 20 percent of digital asset turnover within the EU in 2025.

Business-friendly Environment

The market maturity of the FinTech sector in Germany continues to enable growing business potential in an above-average collaborative FinTech ecosystem in which only seven percent all of FinTech companies consider the competitive situation as being challenging.

The Business Environment for Germany’s FinTech Industry Enables Growth

Talent Pool

Germany has an internationally recognized education system with university and non-university training. The country is also a desirable place to work for people from Europe and further afield.

Financing

A variety of financing options are available within the FinTech sector. Innovative business models are financed in particular by VC donors and corporate VCs but also by other investors and banks. Germany is the third biggest European country in terms of number of start-up investors.

Accelerators and Incubators

Banks, insurance companies and other companies initiate corporate start-up programs and establish accelerator and incubator offices in order to establish new FinTech companies in the market. Some entrepreneurs are also focusing their activities in FinTech.

Coworking

Housing and commercial rents in German cities are relatively moderate compared to international FinTech centers. A wide range of coworking spaces and other flexible solutions are available across the country.

Financial Regulation

The Federal Financial Supervisory Authority (BaFin) brings the supervision of banks, financial service providers, insurance undertakings, and securities trading together under one roof. It is an autonomous public-law institution and is subject to the legal and technical oversight of the Federal Ministry of Finance (BMF). FinTech business models are diverse and may – depending on their structure – require authorization from the Federal Financial Supervisory Authority.

Entrepreneurs and FinTechs can contact the supervisory agency using the BaFin website. Here they can also make preliminary inquiries via a contact form and submit specific questions regarding the specific business model. In order to facilitate companies dealing with supervisory issues, BaFin offers a FinTech-tailored and compact set of current FAQs about FinTech business models on its website:

Digital Hub Initiative

A series of regional digital hubs have been established in Germany as part of an initiative of the German Federal Ministry for Economic Affairs and Energy. Start-ups, science, SMEs, industry, and local administration join together to become centers of digital transformation. The cities of Berlin and Frankfurt are home to one FinTech hub each and the cities of Cologne and Munich each have an InsurTech hub.